E-Invoicing is transforming the way businesses in Malaysia manage their transactions, offering a more efficient, secure, and paperless approach to billing. With the Malaysian government setting July 1, 2024, as the starting date for the implementation of e-Invoicing for all businesses, many are seeking clarity on what this transition entails.

From understanding compliance requirements with LHDN regulations to exploring the benefits it offers, there are numerous questions surrounding this new system. In this article, we’ve compiled a comprehensive FAQ on e-Invoice in Malaysia to address the most common concerns and help businesses prepare for this significant shift.

An e-Invoice is a digital representation of a transaction between a supplier and a buyer, formatted in a structured, machine-readable manner. It is a file created in the format specified by the IRBM (i.e., in XML or JSON file format) and not in the form of PDF, JPG and etc.

The e-Invoice must be generated in the form of XML or JSON file format, in accordance with the requirements outlined by the IRBM. Refer to e-Invoice Software Development Kit (SDK) Microsite via the following link - https://sdk.myinvois.hasil.gov.my for the sample of XML / JSON.

You can streamline your e-Invoicing process with LHDN-compliant solutions like Assist.biz (available Free Lifetime Trial with no commitment) ensuring smooth and hassle-free compliance with Malaysian regulation.

IRBM has provided two (2) e-Invoice transmission mechanisms:

1. Through the MyInvois Portal provided by IRBM; and

2. Application Programming Interface (API).

Taxpayers may use either or both transmission mechanisms to transmit e-Invoices, as long as there is no duplication of e-Invoices.

Note: The e-Invoice model in Malaysia adopts the Continuous Transaction Control (CTC) Model, which enables a high level of control through the validation of e-Invoices received by IRBM.

Failure to comply with this requirement may lead to significant consequences, including penalties or fines imposed by the Inland Revenue Board (IRB). Non-compliance could also result in delays in tax filings, rejection of manual invoices, and difficulties claiming tax refunds, which could disrupt business operations.

No, the issuance of e-Invoice is not limited to only transactions within Malaysia. It is also applicable for cross-border transactions.

Yes, all taxpayers undertaking commercial activities in Malaysia are required to issue e-Invoice, in accordance with the phased mandatory implementation timeline.

Currently, there are no industries that are exempted from the e-Invoice implementation. Note that certain persons and types of income and expense are exempted from e-Invoice implementation.

Currently, there are no industries that are exempted from the e-Invoice implementation. Note that certain persons and types of income and expense are exempted from e-Invoice implementation.

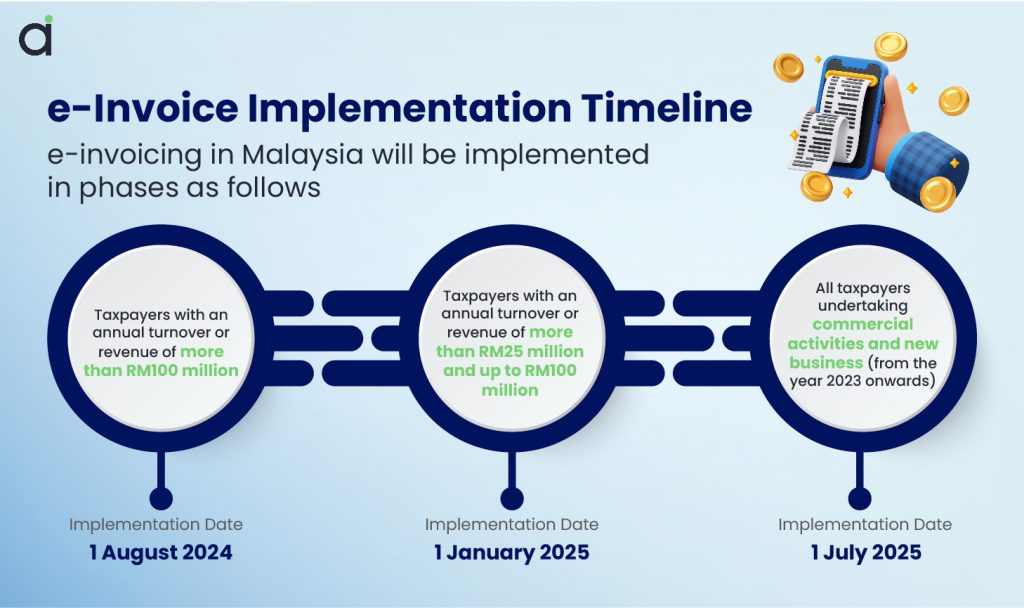

All taxpayers are required to implement e-Invoice. e-Invoice will be implemented in phases according to annual turnover or revenue thresholds as stated in the statement of comprehensive income in the Financial Year 2022 Audited Financial Statements.

Implementation Date Taxpayers with:

- annual turnover or revenue of more than RM100 million 1 August 2024

- Taxpayers with an annual turnover or revenue of more than RM25 million and up to RM100 million 1 January 2025

- All other taxpayers 1 July 2025

When implementing e-Invoice, the three (3) primary factors to consider are:

- Human resources: Businesses are advised to assemble a dedicated team equipped with the necessary expertise and capabilities to prepare for the implementation.

- Business processes: Conduct a comprehensive review of the current process and procedures in issuing invoice transaction documents.

- Technology and systems: Confirm the availability of the necessary resources, data structures and existing IT. capabilities to ensure the systems in place comply with the e-Invoice requirements.

You can streamline your e-Invoicing process with LHDN-compliant solutions like Assist.biz (available Free Lifetime Trial with no commitment) ensuring smooth and hassle-free compliance with Malaysian regulation.

You may contact us through the following channels for any queries or concerns regarding:

- The e-Invoice implementation in Malaysia: myinvois@hasil.gov.my

- Any enquiries (e.g.: Software Development Kit (SDK)): MyInvois Customer Feedback Form at https://feedback.myinvois.hasil.gov.my

Alternatively, taxpayers may reach out to the e-Invois HASiL Help Desk Line at 03-8682 8000, available 24 hours a day, from Monday to Sunday OR chat with us via the MyInvois Live Chat at https://www.hasil.gov.my/en/e-invoice/contact-us.

The Malaysian government has announced the following tax incentives or grants in relation to implementation of e-Invoice during Budget 2024.

Tax deduction of up to RM50,000 for each year of assessment given on environmental, social and governance related expenditure, including consultation fee for the implementation of e-Invoice incurred by Micro, Small, and Medium Enterprises (MSMEs), effective from year of assessment 2024 to year of assessment 2027.

e-Invoice can be displayed in any currency, including RM. Unless there are legal or tax requirements to include the RM-equivalent, taxpayers can issue the e-Invoice in foreign currency. Refer to Section 13 of the e-Invoice Specific Guideline for further details

Kindly note that self-billed e-Invoice is only allowed for certain transactions as stated under Section 8 of the e-Invoice Specific Guideline.

Businesses who are facing poor internet connectivity and lack infrastructure to issue e-Invoice are advised to approach the nearest IRBM state office for further discussions.

Issuance of self-billed e-Invoice is only permitted for circumstances that are provided under the e-Invoice Specific Guideline. Where the transaction does not fall within the e-Invoice Specific Guideline, taxpayers are not allowed to issue self-billed e-Invoice.

Further to harmonisation with Royal Malaysian Customs Department (RMCD), taxpayers are required to input the C3 details when issuing e-Invoice or self-billed e-Invoice, as the case may be.

Yes, where the buyers request for an e-Invoice to be issued, the buyers are required to share their details to the supplier for the purposes of issuing e-Invoice.

For the purposes of e-Invoice, individual taxpayers should provide TIN with prefix of “IG”.

Suppliers are required to obtain buyer’s details from the foreign buyers for the purposes of e-Invoice issuance.

In relation to TIN to be input in the e-Invoice, supplier may use “EI00000000020” for foreign buyers without TIN. Refer to Section 10.5 of the e-Invoice Specific Guideline for further details.

Taxpayers registered with SSM are required to input the new business registration number (12-digit characters) for the purposes of e-Invoice issuance.

However, LHDNM understand that there have been some difficulties for taxpayers to provide the new business registration number from SSM, resulting in validation failures. In response, LHDNM has taken a step to temporarily disable the business registration number validation requirement from the e-Invoice submission process, effective from 19 July 2024.

For taxpayers that are registered with other authority / body, the taxpayers are required to input the relevant registration number.

There is no specific requirement on the timing of e-Invoice issuance, except in specific cases such as consolidated e-Invoice, self-billed e-Invoice for importation of goods / services and e-Invoice for foreign income.

- For consolidated e-Invoice, suppliers are required to issue the consolidated e-Invoice within seven (7) calendar days after the month end.

- For self-billed e-Invoice for importation of goods, the Malaysian purchasers are required to issue self-billed e-Invoice latest by the end of the month following the month of customs clearance is obtained.

- For self-billed e-Invoice for importation of services, the Malaysian purchasers are required to issue self-billed e-Invoice latest by the end of the month following the month upon (1) payment made by the Malaysian purchaser; or (2) receipt of invoice from foreign supplier, whichever earlier. The determination of the aforementioned (1) and (2) is in accordance with the prevailing rules applicable for imported taxable service.

- For e-Invoice for foreign income, the suppliers (i.e., income recipients) are required to issue the e-Invoice latest by the end of the month following the month of receipt of the said foreign income.

Where any specific legislation is applicable, you may proceed to follow as per the said legislation.

Yes, the supplier is allowed to issue consolidated e-Invoice for transactions where no request for e-Invoice has been made by the buyer, regardless of business-to-business (B2B), business-to-consumer (B2C) or business-to-government (B2G) transactions, except for transactions / activities listed under the e-Invoice Specific Guideline.

Yes, the supplier will be able to create e-Invoice in draft or proforma. e-Invoice will only be accepted once the validation is successful.

Failure to issue e-Invoice is an offence under Section 120(1)(d) of the Income Tax Act 1967 and will result in a fine of not less than RM200 and not more than RM20,000 or imprisonment

not exceeding 6 months or both, for each non-compliance.

The e-Invoice validation by IRBM will be done in near real-time, generally in less than two (2) seconds. Refer to the e-Invoice Specific Guideline for further details.

IRBM validation includes a series of checks to ensure the e-Invoice submitted to IRBM conforms to the e-Invoice format and data structure as specified by IRBM. Refer to the e-Invoice SDK Microsite for further details.

Taxpayers are allowed to adopt any format for the visual representation of the e-Invoice as per current practice, provided the QR code is embedded accordingly.

IRBM acknowledges that there may be practical challenges in sharing the validated e-Invoice (in the form of XML / JSON file). Therefore, until further notice, the IRBM allows taxpayers to

share either the validated e-Invoice or a visual representation of the validated e-Invoice, or both.

No, the supplier would need to cancel the e-Invoice within 72 hours from time of validation and reissue a new e-Invoice.

Any changes after 72 hours from time of validation would require the supplier to issue a new e-Invoice (i.e., debit note, credit note, refund note e-Invoice) to adjust the original e-Invoice issued. Thereafter, a new e-Invoice would be required to be issued accordingly.